Key Points

- S&P 500 climbed to a record 6,876.97, up nearly 1% intraday.

- Traders await the Trump–Xi summit for clarity on tariffs and rare earth export curbs.

- Broader risk appetite lifted global equities as gold retreated and Asian indices hit new highs.

The S&P 500 Index edged higher on Monday, rising around 1% intraday to hit another record high near 6,880, supported by optimism that the upcoming U.S.–China trade talks could lead to a de-escalation in tensions.

U.S. officials said negotiators had agreed on a framework that could pave the way for lower tariffs on Chinese imports and concessions on rare earth export limits, spurring a broad rally across risk assets. Global equities followed suit, with Japan’s Nikkei 225, South Korea’s KOSPI, and Taiwan’s TAIEX all reaching fresh peaks, while safe-haven demand for gold eased.

Market Sentiment

Traders are entering this week’s trade discussions with measured optimism and a sense of déjà vu. Past patterns of tariff threats followed by reconciliatory gestures under President Trump’s leadership have kept markets volatile yet resilient.

Analysts have labelled this dynamic the “TACO pattern”: Trump Always Chickens Out. This reflects investor expectations that major threats are often scaled back before deals are finalised.

Still, analysts warn that the market’s upside potential may be limited given elevated valuations and heavy exposure to AI-related stocks.

Global Backdrop

Beyond trade talks, sentiment was lifted by expectations that the Federal Reserve may cut rates this week following softer inflation data, while the Bank of Japan is expected to maintain its accommodative stance.

However, analysts remain wary that earnings softness or any negative surprise from the Trump–Xi meeting could trigger profit-taking.

Technical Analysis

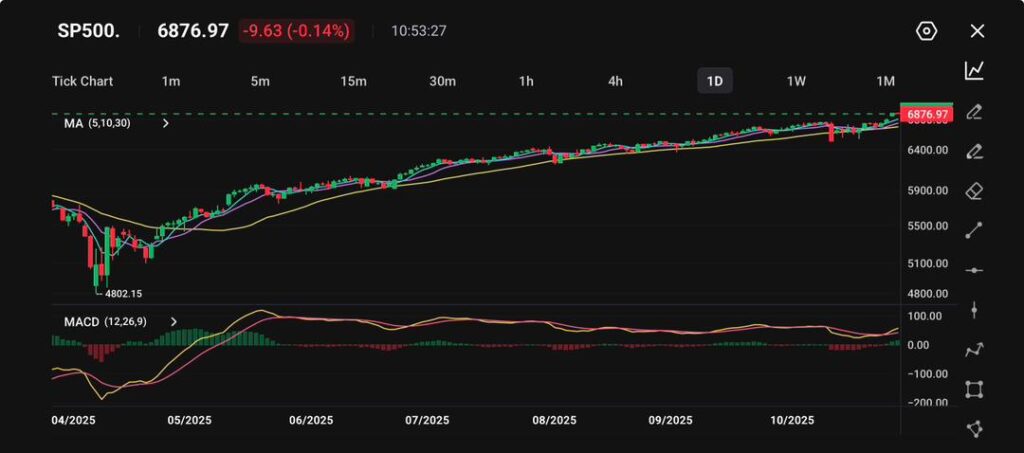

The S&P 500 eased slightly by 0.14% to close at 6,876.97, pausing after an extended multi-month climb that has carried the index to fresh record territory.

The minor dip reflects mild profit-taking ahead of key U.S. macroeconomic releases later in the week, including inflation and employment data that could shape expectations for the Federal Reserve’s next policy move.

From a technical perspective, the index remains in a clear long-term uptrend. The 5-, 10-, and 30-day moving averages continue to align in a bullish formation, supporting the broader market structure.

The index has respected its rising channel since May 2025, with short-term support seen near 6,800, followed by stronger structural support at 6,650. The next upside target remains near 6,950–7,000, where resistance could emerge.

The MACD still signals bullish momentum, albeit with a narrowing spread between the MACD and signal lines, hinting at slowing upside velocity. Histogram bars have begun to flatten, suggesting a period of consolidation rather than reversal. Should momentum resume, a renewed crossover to the upside could reinforce buying pressure.

Fundamentally, sentiment remains underpinned by optimism surrounding AI-driven corporate earnings, resilient U.S. consumption, and easing Treasury yields, which have reduced pressure on equities.

However, traders are watching for any shift in Fed rhetoric that could temper risk appetite if policymakers maintain a “higher-for-longer” stance.

Outlook

The S&P 500’s resilience highlights continued investor confidence in easing trade and policy conditions. However, given the historical pattern of post-summit pullbacks, traders are likely to remain cautious. Attention now turns to the Trump–Xi summit on Thursday and the Federal Reserve’s policy decision, both of which could define near-term direction for global risk assets.